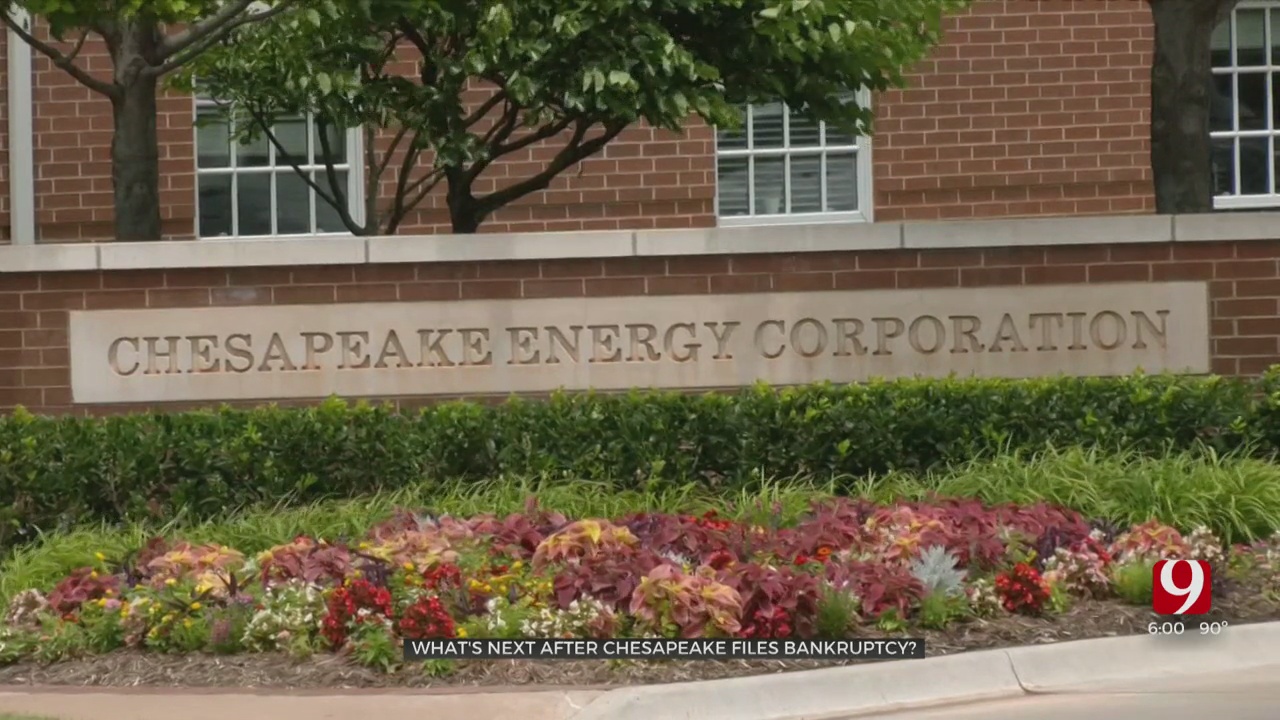

Long Term Debt Brings Chesapeake To Bankruptcy Amid COVID-19 Energy Downturn

After filling Chapter 11 Bankruptcy, Chesapeake Energy stock is frozen as the New York Stock Exchange works to remove one of Oklahoma’s largest energy companies from Wall Street. News 9's Storme Jones has the story.Monday, June 29th 2020, 5:44 pm

OKLAHOMA CITY -

After filling Chapter 11 Bankruptcy, Chesapeake Energy stock is frozen as the New York Stock Exchange works to remove one of Oklahoma’s largest energy companies from Wall Street.

“Most of the root problem here is the enormous debt that was built up over time, certainly when Aubrey McClendon was still CEO they had accrued about $21 billion worth of debt,” Dean of OCU’s Minders School of Business Steve Agee said.

The approximately $21 billion in debt amassed before McClendon’s departure in 2013 was roughly the same debt load carried by much larger Chevron and Exon Mobile combined at the time.

A person familiar with workings of the company said Chesapeake had “no formal budgeting process” under the wildcatter billionaire executive.

Since taking over in 2013, current CEO Doug Lawler has brought the legacy debt load down to around $9 billion.

In March, a fight between Saudi Arabia and Russia increased supply and COVID-19 dropped demand, compounding issues with existing debt.

“With the oil and natural gas prices the way they are right now, it would be almost impossible for them to dig their way out of that situation,” Agee said.

The bankruptcy agreement filed in the U.S. Southern District of Texas aims to take debt down to around $2 billion.

“That might involve additional cuts in terms of employment, it might involve trying to get out of agreements that they’ve already signed up on like the Chesapeake Arena agreement,” Agee said

“This is a financial restructuring, and we will continue to operate our business as usual,” Lawler told employees in a Sunday letter. “You will continue to be paid and receive benefits.”

The company said it has secured $600 million in new investments to help on the other side of bankruptcy.

“Long term I think Chesapeake has a very viable, sustainable future they were just caught up in a terrible situation with this COVID crisis,” Agee said.

Get The Daily Update!

Be among the first to get breaking news, weather, and general news updates from News 9 delivered right to your inbox!

More Like This

March 8th, 2022

January 21st, 2022

January 13th, 2022

Top Headlines

April 19th, 2024

We Remember: City, State Leaders Expected To Assemble For Oklahoma City Bombing Remembrance Ceremony

We Remember: City, State Leaders Expected To Assemble For Oklahoma City Bombing Remembrance Ceremony

April 19th, 2024

April 19th, 2024