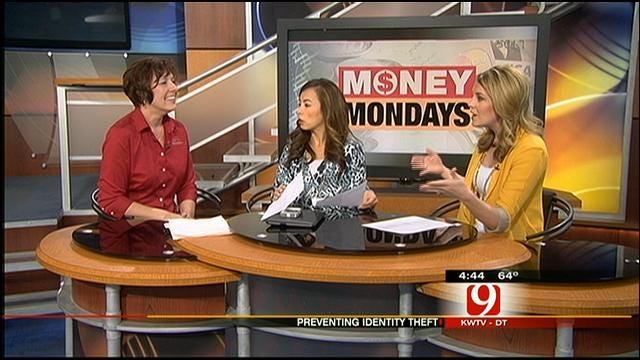

Money Monday: Identity Theft

Financial expert, Cynthia Campbell, shares some answers to some common questions about identity theft and how to protect ourselves.Monday, October 8th 2012, 6:25 pm

Fifteen million people will be victims of identity theft this year. Financial expert, Cynthia Campbell, shares some answers to some common questions about identity theft and how to protect ourselves.

Q: What is identity theft?

A: Identity Theft occurs when someone uses your personal information to commit fraud or other crimes. When the identity is stolen for the purpose of financial fraud we see new accounts created and existing accounts penetrated. Identities are also stolen for non-financial reasons such as the use of others medical insurance and the use of others access to places and information (pre-texting / social engineering).

Q: How prevalent is the crime of identity theft?

A: Identity theft has been the top consumer complaint to the Federal Trade Commission for 12 years in a row. In 2011, we saw identity increase by 13%, as you can imagine in a struggling economy identity theft increases. Most think that senior citizens are the most targeted group but in fact it is the other end of the spectrum that we should be most concerned about because they are the hardest hit. They may be the target because young adults, aged 18-24, took the longest to detect identity theft - 132 days on average - when compared to other age groups. Subsequently, the average cost ($1,156) was roughly five times more than the amount lost by other age groups. Seniors are the second highest group targeted.

Q: How can we prevent identity theft?

A: The number one key to preventing identity theft is to keep your key information private!

- • Keep all identification and financial documents in a safe and private place

- • Provide personal information only when: You know how will be used / You are certain it won't be shared / You initiated contact and know who you're dealing with

- • Make all passwords hard to guess by using a complex combination of numbers and upper and lower case letters

- • Mail: Request a vacation hold if you can't pick up your mail / Don't put outgoing mail in your mailbox drop it off at the PO / Remove mail from your mailbox promptly

- • Phones: Seven percent of Smartphone owners were victims of identity fraud. This incidence rate is one-third higher than that of the general public. 32% of Smartphone owners do not update to a new operating system when it becomes available; 62% do not use a password on their home screen, thus allowing easy access to information if the phone is lost; 32% save login information on their mobile device.

- • Keep your purse or wallet in a safe place at work

- • Like we talked about last week, periodically check your credit report and dispute inaccurate information immediately. The credit report (or a collection call) are the two ways most folks find out they are a victim.

Q: What if we do become victims, how do we recover?

A: Communication with authorities. The average victim spends about 40 hours cleaning up the mess caused by identity thieves.

- • Contact your creditors and your financial institution immediately. Most have specialist that will assist you in recovery.

- • Report the crime to the police department, they may also ask you to complete a uniform affidavit from the Federal Trade Commission's website to accompany your police report. Your creditors may want copies of these reports to complete the recovery.

- • Place a fraud alert (available via the credit bureaus) on your credit report to prevent further damage.

- • Change ALL passwords!

Get The Daily Update!

Be among the first to get breaking news, weather, and general news updates from News 9 delivered right to your inbox!

More Like This

October 8th, 2012

March 22nd, 2024

March 14th, 2024

February 9th, 2024

Top Headlines

April 19th, 2024

April 19th, 2024

April 19th, 2024

April 19th, 2024